Table of Contents

पुनर्मुल्यांकन खाता(Revaluation Account)

पुनर्मुल्यांकन खाता एक नाममात्र का खाता है यह खाता सम्पत्तियों के पुनर्मूल्यांकन (Revaluation) तथा दायित्वों के पुनर्निर्धारण (Re-assessment) पर होने वाले लाभ अथवा हानि को ज्ञात करने उद्देश्यसे बनाया जाता है। सम्पत्तियों के पुनर्मूल्यांकन तथा दायित्वों के पुनर्निर्धारण पर होने वाले लाभ अथवा हानि को पुराने साझेदारों में उनके लाभ विभाजन अनुपात (Profit Sharing Ratio) में बाँट दिया जाता है।

जब नया साझेदार साझेदारी प्रवेश (Admission) में करता है या कोई पुराना साझेदार साझेदारी से अवकाश ग्रहण(Retirement) करता है या किसी पुराने साझेदार की मृत्यु ( Death) हो जाती है तो फर्म सम्पत्तियों का पुनर्मूल्यांकन (Revaluation) तथा दायित्वों का पुनर्निर्धारण (Re-assessment) करना आवश्यक हो जाता है इस उद्देश्य की फर्म की पुस्तकों में एक नया खाता खोला जाता है जिसे पुनर्मुल्यांकन खाता (Revaluation Account) कहा जाता है।

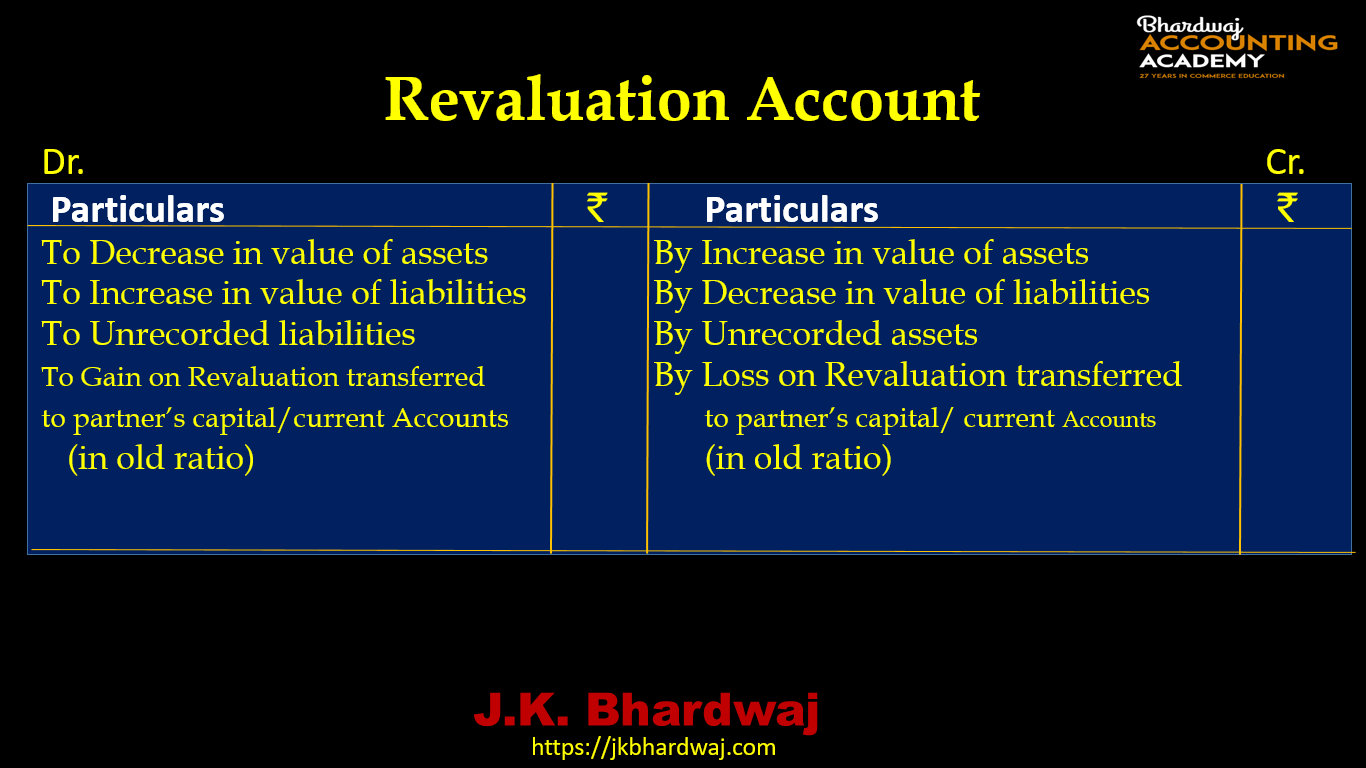

- सम्पत्तियों में मूल्य में होने वाली वृद्धि को पुनर्मुल्यांकन खाते में जमा (Credit) किया जाता है।

- सम्पत्तियों में मूल्य में होने वाली कमी को पुनर्मुल्यांकन खाते में नाम(Debit) किया जाता है।

- दायित्वों में मूल्य में होने वाली कमी को पुनर्मुल्यांकन खाते में जमा(Credit) किया जाता है।

- दायित्वों में मूल्य में होने वाली वृद्धि को पुनर्मुल्यांकन खाते में नाम(Debit) किया जाता है।

- बिना लिखी सम्पत्तियों को पुनर्मुल्यांकन खाते में जमा(Credit) किया जाता है।

- बिना लिखे दायित्वों को पुनर्मुल्यांकन खाते में नाम(Debit) किया जाता है।

- ऐसे दायित्व से समाप्त हो गये हैं उन्हैं पुनर्मुल्यांकन खाते में क्रेडिट पक्ष (Credit side) में लिखा जाता है।

- ऐसी सम्पत्तियाँ जिनका कोई मूल्य नहीं रह गया( Value Less) है उन्हैं पुनर्मुल्यांकन खाते में डेबिट पक्ष ( Debit side) में लिखा जाता है।

- सम्पत्तियों के पुनर्मुल्यांकन पर होने वाले लाभ को पुनर्मुल्यांकन खाते में जमा(Credit) किया जाता है और हानि को नाम(Debit) किया जाता है।

- दायित्वों के पुनर्निर्धारण पर होने वाले लाभ को पुनर्मुल्यांकन खाते में जमा(Credit) किया जाता है और हानि को नाम(Debit)किया जाता है।

- पुनर्मुल्यांकन खाते को लाभहानि समायोजन खाते (Profit and Loss Adjustment Account) के नाम से भी जाना जाता है।

- सम्पत्तियों के पुनर्मूल्यांकन तथा दायित्वों के पुनर्निर्धारण पर होने वाले लाभ अथवा हानि को पुराने साझेदारों में उनके लाभविभाजन अनुपात में बाँट दिया जाता है और पूँजी अथवा चालू खातेे में हस्तान्तरित कर दिया जाता है।

Bhardwaj Accounting Academy: Home

पुनर्मुल्यांकन खाता

सम्पत्तियों के पुनर्मूल्यांकन तथा दायित्वों के पुनर्निर्धारण पर की जाने वाली प्रविष्टियाँ या लेखे

(Accounting Entries on Revaluation of assets and Re-assessment of lialilities)

1.सम्पत्तियों के मूल्य में वृद्धि होने पर

Asset A/c Dr. (individually)

To Revaluation A/c

[Increase in the value of Asets]

2.सम्पत्तियों के मूल्य में कमी होने पर

Revaluation A/c Dr. (individually)

To Asset A/c

[Decrease in the value of assets]

3.दायित्यों के मूल्य में वृद्धि होने पर

Revaluation A/c Dr. (individually)

To Liabilities A/c

[Increase in the value of Liabilities]

4.दायित्वों के मूल्य में कमी होने पर

Liabilities A/c Dr.

To Revaluation A/c

[Decrease in the value of Liabilities]

5.बिना लिखे दायित्व को हिसाब में लेने पर

Revaluation A/c Dr.

To Liability A/c [unrecorded]

[Unrecorded Liability recorded at actual value]

6.बिना लिखी सम्पत्ति को हिसाब में लेने पर

Asset A/c [unrecorded] Dr.

To Revaluation A/c

[Unrecorded asset recorded at actual value]

7.डूबतऋण प्रावधान में वृद्धि होने पर

Revaluation A/c Dr.

To Provision for doubtful debts A/c

[Provision for doubtful debts created on debtors]

8.डूबतऋण प्रावधान में कमी होने पर

Provision for doubtful debts A/c Dr.

To Revaluation A/c

[Provision for doubtful debts decrease]

9. (a) डूबत ऋण को अपलिखित करने पर

Bad debts A/c Dr.

To Debtors A/c

[Bad debts written off]

(b) डूबत ऋण को पुनर्मूल्यांकन खाते में डेबिट करने पर

Revaluation A/c Dr.

To Bad debts A/c

[Bad debts transfer to Revaluation account]

10.पुनर्मूल्यांकन पर लाभ होने पर

Revaluation A/c Dr.

To Existing Or Old Partner’s Capital/Current A/c

[Profit on revaluation transferred to capital/current account in existing ratio]

11.पुनर्मूल्यांकन पर हानि होने पर

Existing Or Old Partner’s Capital/Current A/c Dr.

To Revaluation A/c

[Loss on revaluation transferred to capital/current account in existing ratio]

ALSO READ : REALISATION ACCOUNT

पुनर्मूल्यांकन खाते का प्रारूप (Format Of Revaluation Account)

ALSO READ : REVALUATION ACCOUNT/ PROFIT & LOSS ADJUSTMENT ACCOUNT