Table of Contents

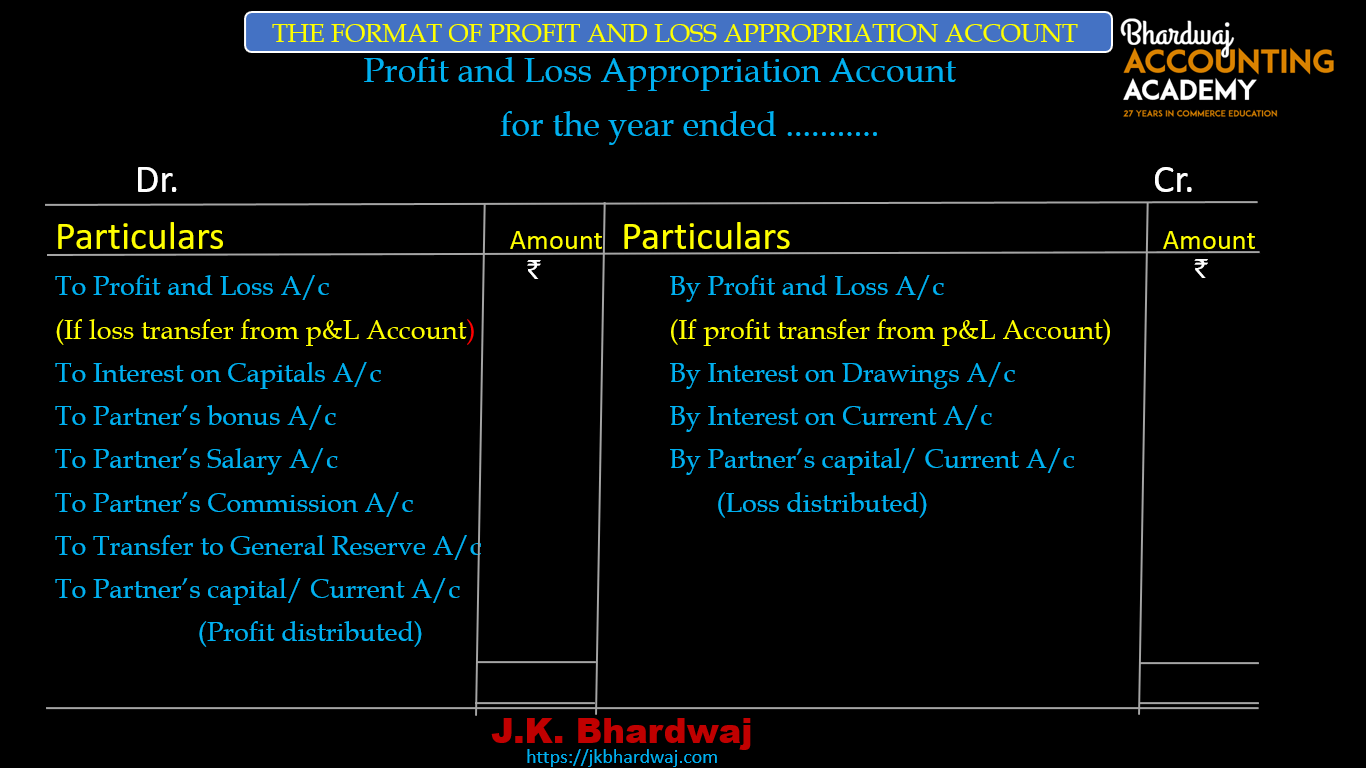

Format of Profit and loss Appropriation Account

Profit and loss Appropriation account-

*Profit and loss Appropriation account is an extension of Profit and Loss account.

*Profit and loss Appropriation account is a special type of account.

*Profit and loss Appropriation account is Prepared after preparing Profit and Loss Account.

*It is prepared to distribute the profits/Losses among the partners. (According to their profit sharing ratio)

*This account is prepared on the basis of partnership deed or agreement.

*This account is prepared by partnership firms only.

*No use of this account for income tax purposes.

*All the appropriations like Interest on capital, Partner’s salaries, Partner’s fees, Partner’s commission, Partner’s bonus, transfer to reserve etc. are recorded on the debit side of this account.

*The net profit (transfer from profit and loss account), interest on drawings, Interest on Current Account (charged on Debit balance of current account) are recorded on the credit side of this account.

*Reserves required for the future are created from this account.

*To prepare it, at first, the balance of Profit and Loss Account is transferred to this account.

*This account is credited with the amount of net profit and debited with the amount of net loss.

ALSO READ : Partnership Deed

The debit side of this account records:

1.Interest on Capital

2.Partners Salary

3.Partners Fees

4.Partners Commission

5.Partners Bonus

6.Transfer to General Reserves

The credit side of this account records:

- Interest on drawings

- Interest on Current Account (Charged on debit Balance)

Purpose Of Profit And Loss Appropriation Account-

i.To know the distribution of profit among partners.

ii.To show how much is payable to partners in the form of salary, bonus, fees, commission , interest on capital etc. these all are debited to Profit and Loss Appropriation Account.

iii.To show how much interest on drawings Charged on partner’s drawings at the credit side of the Profit and Loss Appropriation Account.

iv.To create reserve from the profits for future.

v.To distribute the profits among the partners in profit sharing ratio.

vi.To distribute the Losses among the partners in profit sharing ratio.

The journal entries for the preparation of Profit and Loss Appropriation Account are given below:

- For transfer of the balance of Profit and Loss Account to Profit and Loss Appropriation Account

(a) In case of Net Profit :

Profit and Loss A/c Dr.

To Profit and Loss Appropriation A/c

(Net Profit transferred to Profit and Loss Appropriation A/c)

(b) In case of Net Loss :

Profit and Loss Appropriation A/c Dr.

To Profit and Loss A/c

(Net Loss transferred to Profit and Loss Appropriation A/c)

- For For Interest on Capital transferring

Profit and Loss Appropriation A/c Dr.

To Interest on Capital A/c

(Interest on capital transferred to Profit & Loss Appropriation A/c)

- For Interest on Drawings transferring

Interest on Drawings A/c Dr.

To Profit and Loss Appropriation A/c

(Interest on drawing transferred to Profit & Loss Appropriation A/c)

- For transfer of partner’s Salary/Bonus

Profit and Loss Appropriation A/c Dr.

To Partner’s Salary / Bonus A/c

(Salary/Bonus transferred to profit & Loss Appropriation A/c)

- For Partner’s Commission transferring

Profit and Loss Appropriation A/c Dr.

To Partner’s Commission A/c

(Commission transferred to Profit and Loss Appropriation A/c)

- For Transfer of agreed amount to General Reserve

Profit and Loss Appropriation A/c Dr.

To General Reserve A/c

(Transfer to General Reserve)

7. For share of Profit or Loss transfer to Partner’s capital/current A/c

(a) If Profit

Profit and Loss Appropriation A/c Dr.

To Partner’s Capital/Current A/c

(Profit transferred to Partner’s capital/current A/c)

(b) If Loss

Partner’s Capital/ Current A/c Dr.

To Profit and Loss Appropriation A/c

(Loss transferred to Partner’s capital/current A/c)

ALSO READ : Format of Profit And Loss Account

Format of Profit and loss Appropriation Account-

ALSO READ : Law Of Supply

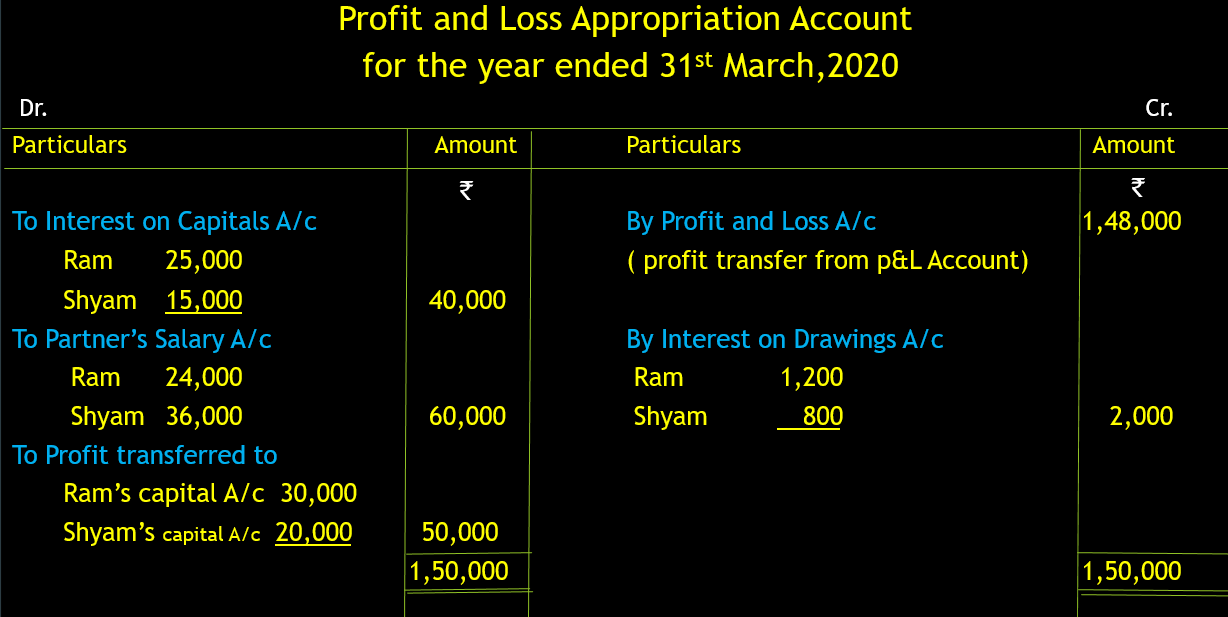

For Example-

Ram and Shyam started a partnership business on 1st April, 2019. Their capital contributions were Rs.2,50,000 and Rs.1,50,000 respectively. The partnership deed provided:

- i. Interest allowed on capitals @10% p.a.

- Ram, get a salary of Rs.2,000 p.m. and Shyam Rs.3,000 p.m.

iii. Profits are to be shared in the ratio of 3:2.

- Their Drawings are Rs. 30,000 and Rs. 20,000 respectively

- Interest charged on Drawings amounted to Rs.1,200 for Ram and Rs. 800 for Shyam.

The profits for the year ended 31st March, 2020 before making above appropriations were Rs. 1,48,000. Prepare Profit and Loss Appropriation Account.

ISC 12 fundamentals of partnership questions (previous papers)