Table of Contents

Users of Accounting Information

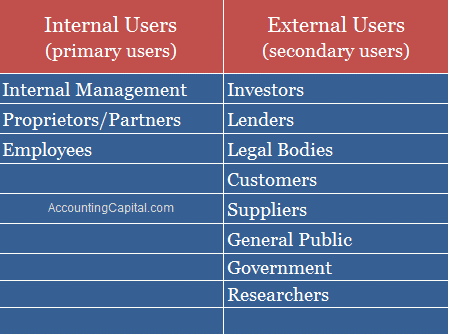

Accounting information is used by various groups of people to take important decisions. These users may be categorized into Internal Users and External Users of accounting.

Internal Users of accounting

Internal users of accounting are that individual who runs, manages and operates the daily activities of the inside area of an organization.

(i) Owners:

Owners are exposed to the maximum risk in the business as they invest capital in the business. So, they are always interested in the safety of the invested capital.

- They also want to know the profitability and financial soundness of the business.

- Accounting information provides them the information about the financial performance of the business.

(ii) Management:

Accounting information is used by the management for taking various decisions. Management is also concerned with ensuring that the money invested in the organization is generating an adequate return and that the organization is able to pay its debts and remain solvent

(iii) Employees:

They are interested in the financial statements to assess the ability of the business to pay higher wages and bonuses. Employees are also interested in knowing whether the various amounts due to them such as Provident Fund, Employees State Insurance, etc are being deposited regularly

Also Read: Basis of Accounting: Cash and Accrual

External Users of accounting

External users of accounting are those individuals who take interest in the account information of a company but they are not part of the company’s administrative process. External users have direct or indirect relation with accounting information.

(i) Banks and Financial Institutions:

Banks and other financial institutions provide loans to the business. So, they need accounting information to ensure the safety and recovery of the loan advanced and regularity of the interest amount

(ii) Investors and Potential Investors:

Present investors use accounting information as they are interested in knowing the earning capacity of the business and the safety of the investment. Prospective investors use the accounting information to assess whether or not to invest their money in the organization.

(iii) Creditors:

They provide goods on credit to the business. So, they need accounting information to ascertain the financial soundness of the firm and to ensure the creditworthiness of the firm.

(iv) Government and their Agencies:

The Government authorities collect various taxes from the business. So, the government needs accounting information to assess the tax liability of the business entity They also need accounting information to regulate the activities of the enterprise and to compile national income accounts.

(v) Researchers:

They use accounting information to undertake research in various economic, business, and other related areas.

(vi) Consumers:

They are interested in getting good quality goods at reasonable prices. So, they require accounting information for establishing good accounting control, which will reduce the cost of production and less price is to be paid by them.

(vii) Public:

Business is an indispensable part of the society and gets its manpower and other resources from society The general public is interested in its accounting information to know the contribution of business towards the welfare of the society

Image Source: Accountingcapital.com

Comments are closed.