Table of Contents

ISC 12 Issue and Redemption of Debentures Questions For Practice

ISC 12 Issue and Redemption of Debentures Questions For Practice

Question 1.

On 1st April, 2021, Bhim Ltd. issued 2,000, 5% Debentures of ₹100 each as follows:

(a) For cash at a discount of 5% ₹ 80,000 (Nominal Value)

(b) To a vendor for 60,000 in satisfaction of his claim ₹ 70,000 (Nominal Value)

(c) To Bankers for a loan of 40,000 as collateral security ₹ 50,000 (Nominal Value)

The interest on these debentures was to be paid annually on 31st March every year by the company. You are required to calculate interest on these debentures payable by the company on 31st March, 2022. [ISC 2023]

Question 2.

On 1st April, 2022, Lighthouse Ltd. purchased land from Bricks Ltd. The payment made on the same day by:

(i) Issuing a bank draft for ₹20,00,000;

(ii) Drawing a Promissory Note in favour of Bricks Ltd. for ₹10,00,000;

(iii) Issuing 8,000, 10% Debentures of ₹100 each at par, redeemable at a premium of 10%, after three years.

You are required to pass necessary journal entries in the books of Lighthouse Ltd. the date of purchase of land. [ISC 2023]

ISC 12 Issue and Redemption of Debentures Questions For Practice

Question 3.

Jerome Ltd., an unlisted manufacturing company, had 20,000, 6% Debentures of ₹100 each due for redemption at par on 31st March, 2022. On this date the company had the required amount of ₹2,00,000 in its Debenture Redemption Reserve.

The Debenture Redemption Investment which was purchased on 30th April, 2021, was realised at 98% on the date of redemption and the debentures were redeemed on the due date.

You are required to pass journal entries in the books of the company for the year 2021-22. (Ignore interest on debentures). [ISC 2023]

Question 4.

On 1st April, 2017, Gabriel Ltd., a listed company, issued 3,000, 8% Debentures of ₹100 each. One-third of the Debentures were redeemed at par on 31st March, 2021, and the remaining two-third on 31st March, 2022.

The company paid interest on debentures annually on 31st March. After meeting the requirements of the Companies Act, 2013, regarding Debenture Redemption Investment, the debentures were redeemed by the company.

You are required to record necessary journal entries in the books of the company only on 31st March, 2022, including entries for interest on debentures. [ISC 2023]

ISC 12 Issue and Redemption of Debentures Questions For Practice

ISC 12 Issue of Shares Questions Previous Papers

Question 5.

Gabby Ltd. (a listed NBFC) has 30,000, 5% Debentures of ₹100 each due for redemption at par on 31st March, 2022.

The Debenture Redemption Investment which was purchased on 30th April, 2021, was realized on the date of redemption at 102% less 0·5% brokerage, and the debentures were redeemed.

You are required to calculate the sale price of the Debenture Redemption

Investment. (ISC SPECIMEN QUESTION PAPER 2023)

Question 6.

On 31st March, 2021, the books of Pragya Ltd. (an unlisted manufacturing company) showed the following closing balances:

7% Debentures (redeemable on 30th September, 2022) ₹ 60,00,000

Debenture Redemption Reserve ₹ 2,00,000

In order to meet the provisions of the Companies Act, 2013, the company transferred the required balance amount to Debenture Redemption Reserve Account on 31st March, 2022. It met the requirements of Debenture Redemption Investment.

You are required to prepare the Debenture Redemption Reserve Account for the years

2021-22, 2022-23. (ISC SPECIMEN QUESTION PAPER 2023)

ISC 12 Issue and Redemption of Debentures Questions For Practice

Question 7.

Barua Ltd. (a listed NBFC) redeems its 9,000, 10% Debentures of ₹ 100 each in instalments

as follows

Date of Redemption Debentures to be redeemed

31st March, 2020 3,000

31st March, 2021 5,000

31st March, 2022 1,000

You are required to prepare the Debenture Redemption Investment Account for the

years 2020-21, 2021-22. (ISC SPECIMEN QUESTION PAPER 2023)

ISC 12 Issue and Redemption of Debentures Questions For Practice

Question 8.

On 1st February, 2022, Swadesh Ltd. issued to the public 12,000, 10% Debentures of ₹ 100

each at a discount of 3% payable:

₹ 20 on application.

The balance on allotment being made on 1st May, 2022.

The public applied for 20,000 debentures. Pro-rata allotment was made on 15,000

debentures.

The debentures were to be redeemed at par after four years.

You are required to pass journal entries for the year 2021-2022. (ISC SPECIMEN QUESTION PAPER 2023)

ISC 12 Issue and Redemption of Debentures Questions For Practice

Question 9.

On 1st April, 2013, Rayon Ltd. issued 2,000, 9% Debentures of ₹ 100 each at a discount of 10%, redeemable at par on 31st March, 2017. The issue was fully subscribed.

To meet the provisions of the Companies Act, 2013, the Board of Directors decided to transfer ₹ 30,000 to Debenture Redemption Reserve on 31st March, 2014, and the balance on 31st March, 2015. On 1st April, 2016, the company made the required investment in government securities.

The investments were encashed and the debentures were redeemed on the due date.

It is the policy of the company to write off capital losses in the year in which they occur. You are required to pass journal entries for issue and redemption of debentures (ignore interest on debentures). [ISC 2018]

ISC 12 Issue and Redemption of Debentures Questions For Practice

Question 10.

On 1st April, 2016, Krayon Ltd. issued 8,000, 12% Debentures of ₹ 100 each, redeemable at par after 5 years. The issue was fully subscribed.

According to the terms of issue, interest on debentures is payable annually on 31st March. Tax deducted at source is 20%.

You are required to pass journal entries for the year 2016-17, regarding issue of debentures and interest on debentures. [ISC 2018]

ISC 12 Issue and Redemption of Debentures Questions For Practice

Question 11.

On 31st March, 2018, Vipul Ltd. had ₹ 30,00,000, 8% Debentures of ₹ 100 each outstanding.

On 1st June, 2018, it purchased in the open market, 20,000 of its own debentures @ ₹ 102 per debenture and cancelled these debentures immediately.

On 31st December, 2018, the remaining debentures were purchased @ ₹ 98 per debenture for immediate cancellation.

You are required to pass necessary journal entries for the redemption of debentures. (Ignore interest on debentures and entries for provisions regarding Debenture Redemption Reserve and Debenture Redemption Investment). [ISC 2019]

ISC 12 Issue and Redemption of Debentures Questions For Practice

Question 12.

You are required to pass journal entries to record the following issues of

debentures and to write off any capital losses.

(a) Zoom Ltd. issues 6,000, 12% Debentures of ₹ 100 each at par redeemable after 5 years also at par.

(b) Zola Ltd. issues 5,000, 13% Debentures of ₹ 100 each at a discount of 10% to be redeemed at par after 7 years.

(c) Zubic Ltd issues 11% Debentures of the total face value of ₹ 12,00,000 at a premium of 5% to be redeemed at par after 6 years.

(d) Ruby Ltd. issues ₹ 5,00,000, 12% Debentures at a premium of 5% to be redeemed at 10% premium after 10 years.

(e) Emerald Ltd. issues 3,000, 9% Debentures of ₹ 100 each at a discount of 7%, to be redeemed at a premium of 10% after 4 years.

Note: All the companies write off their capital losses in the year in which they occur. [ISC 2019]

ISC 12 Issue and Redemption of Debentures Questions For Practice

Question 13.

Zee Ltd. purchased a running business from Rainbow Ltd. for a sum of ₹ 6,60,000. Zee Ltd. paid 5% of the purchase consideration by drawing a Promissory Note in favour of Rainbow Ltd. and the balance by the issue of fully paid 7% Debentures of ₹ 100 each at a premium of 10%. The assets and liabilities of Rainbow Ltd. consisted of:

Fixed Assets (₹)6,50,000

Sundry Creditors (₹)80,000

You are required to pass the necessary journal entries in the books of Zee Ltd. [ISC 2020]

ISC 12 Issue and Redemption of Debentures Questions For Practice

Question 14.

On 1st April, 2016, the following balances appeared in the books of Shikhar Ltd.

10% Debentures ₹ 14,00,000

Premium on Redemption of Debentures ₹ 1,40,000

Debenture Redemption Reserve ₹ 75,000

The debentures were to be redeemed at a premium of 10% in two equal annual installments beginning from 31st March, 2018. To meet the requirements of the Companies Act, 2013, the company transferred the balance amount to Debenture Redemption Reserve on 31st March, 2017.

On 30th April, 2017, it met the requirements of the Companies Act, 2013 regarding Debenture Redemption Investment and redeemed the debentures on the scheduled dates.

You are required to pass necessary journal entries to record the above

transactions in the books of Shikhar Ltd. (Ignore interest on Debentures). [ISC 2020]

ISC 12 Issue and Redemption of Debentures Questions For Practice

Question 15.

On 1st April, 2015 Max Ltd. took over assets of ₹4,50,000 and liabilities of ₹ 60,000 of Prudence Ltd. for the purchase consideration of ₹4,40,000. It paid the purchase consideration by issuing 8% Debentures of ₹100 each at 10% premium.

On the same date it issued another 3,000 8% Debentures of ₹100 each at a discount of 10%, redeemable at a premium of 5% after 5 years. According to the terms of the issue ₹30 is payable on application and the balance on the allotment of debentures.

You are required to pass journal entries in the books of Max Ltd. to record the above

transactions. [ISC SPECIMEN QUESTION PAPER – 2017]

ISC 12 Issue and Redemption of Debentures Questions For Practice

MEANING OF DEBENTURES:

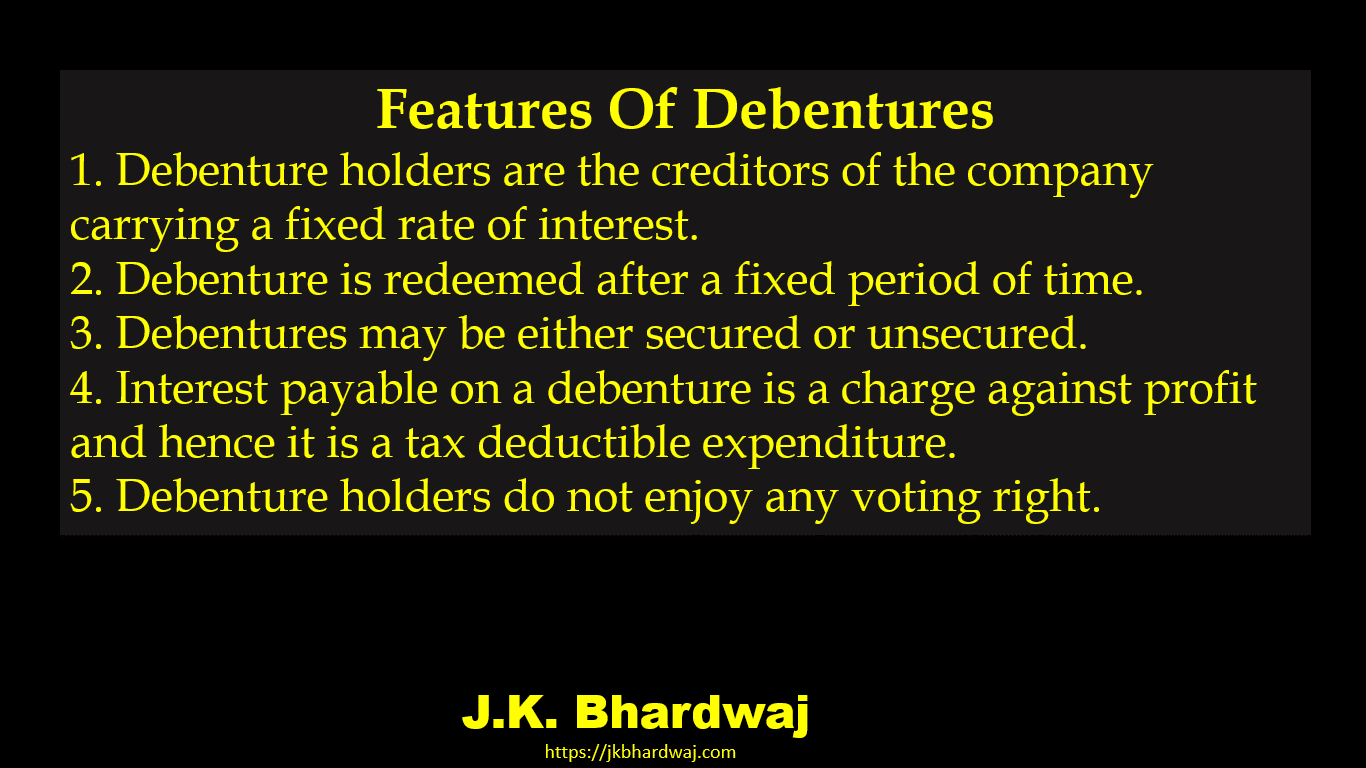

FEATURES OF DEBENTURES:

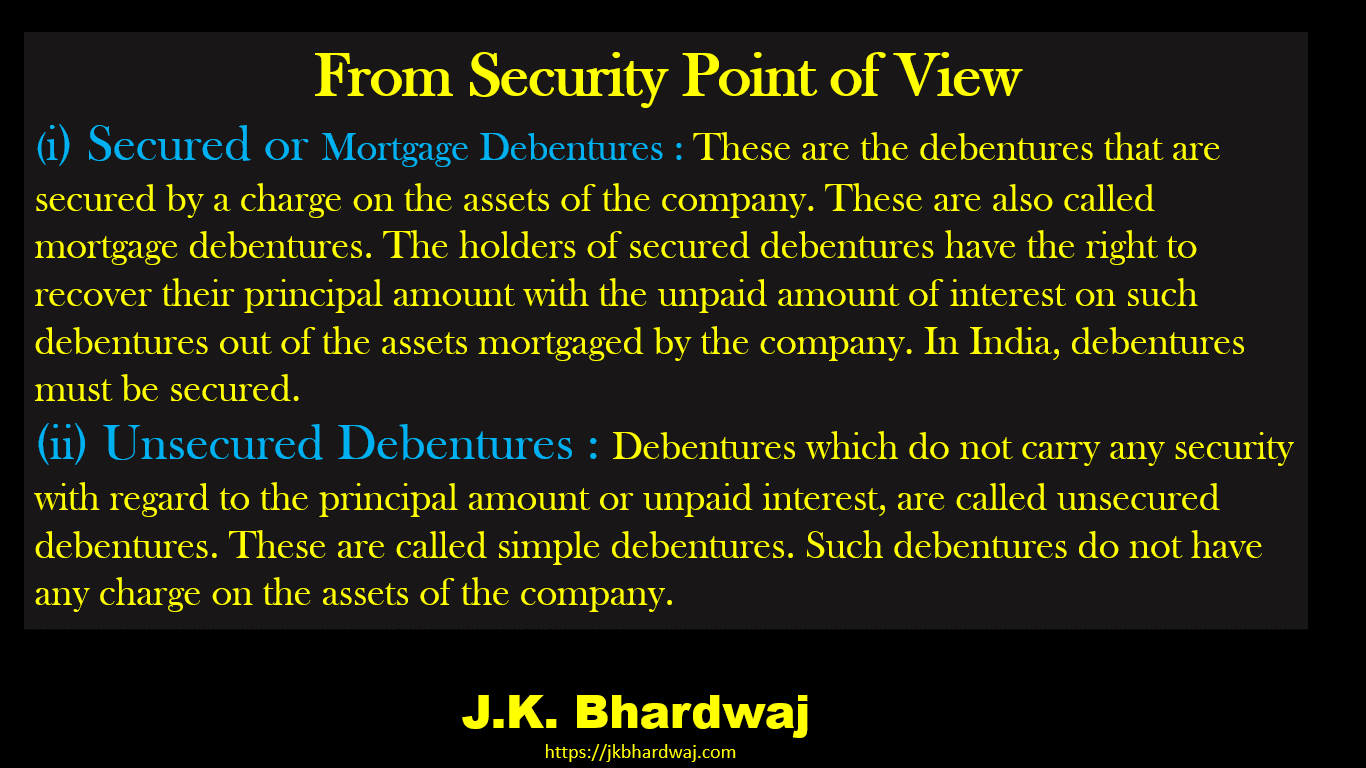

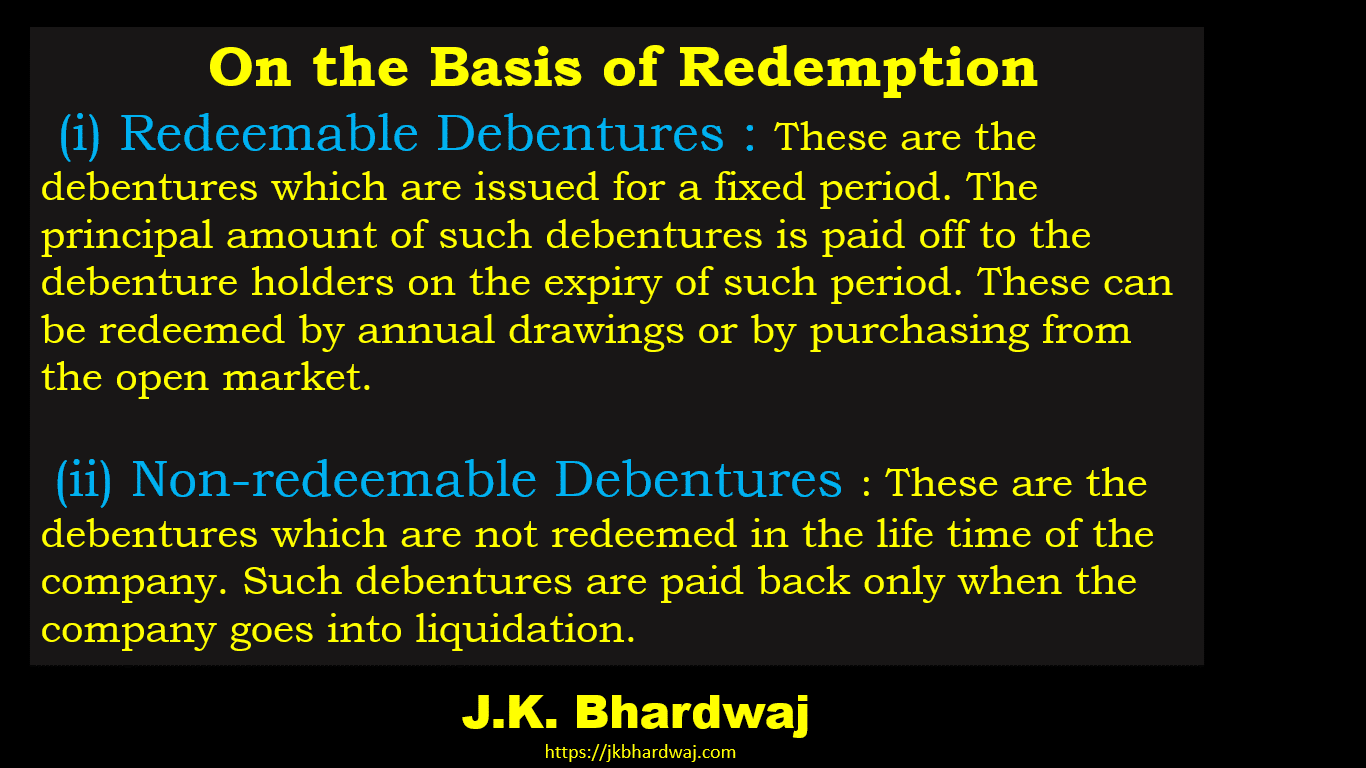

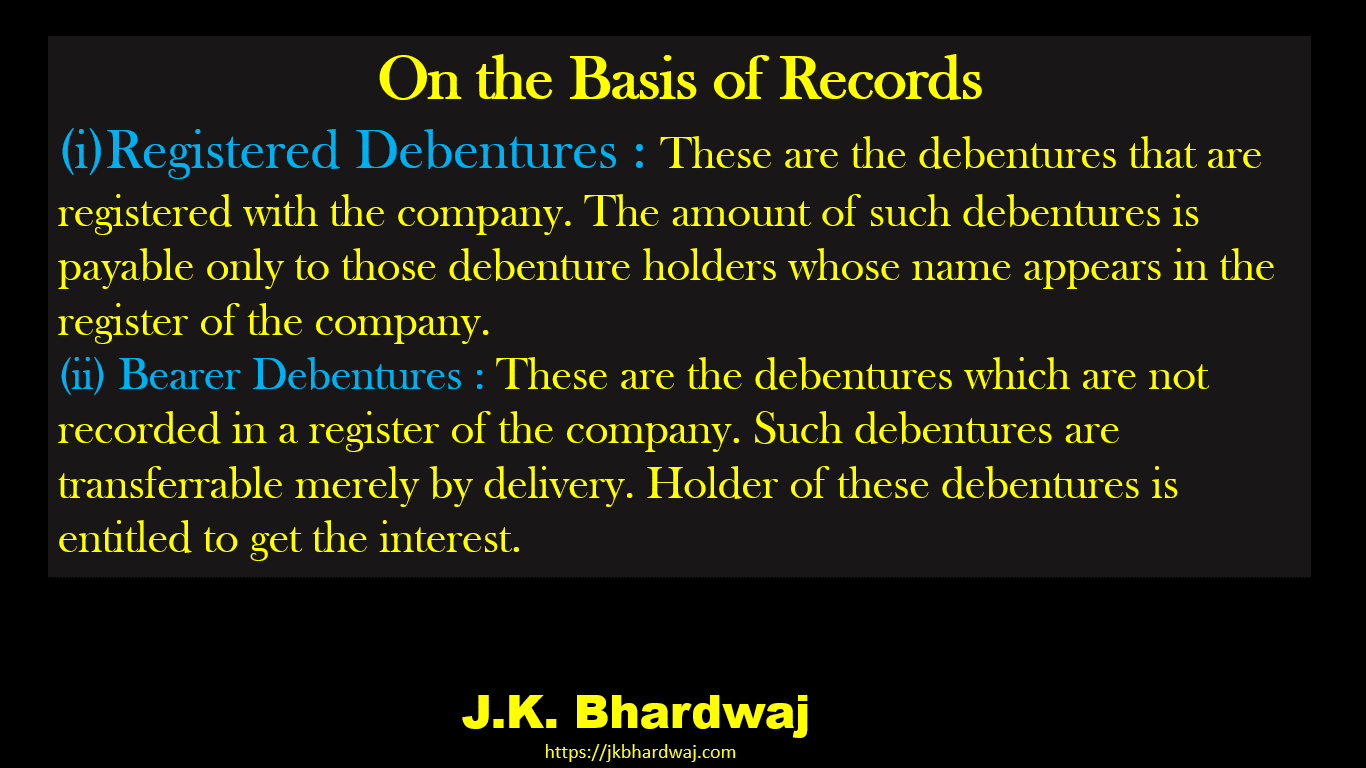

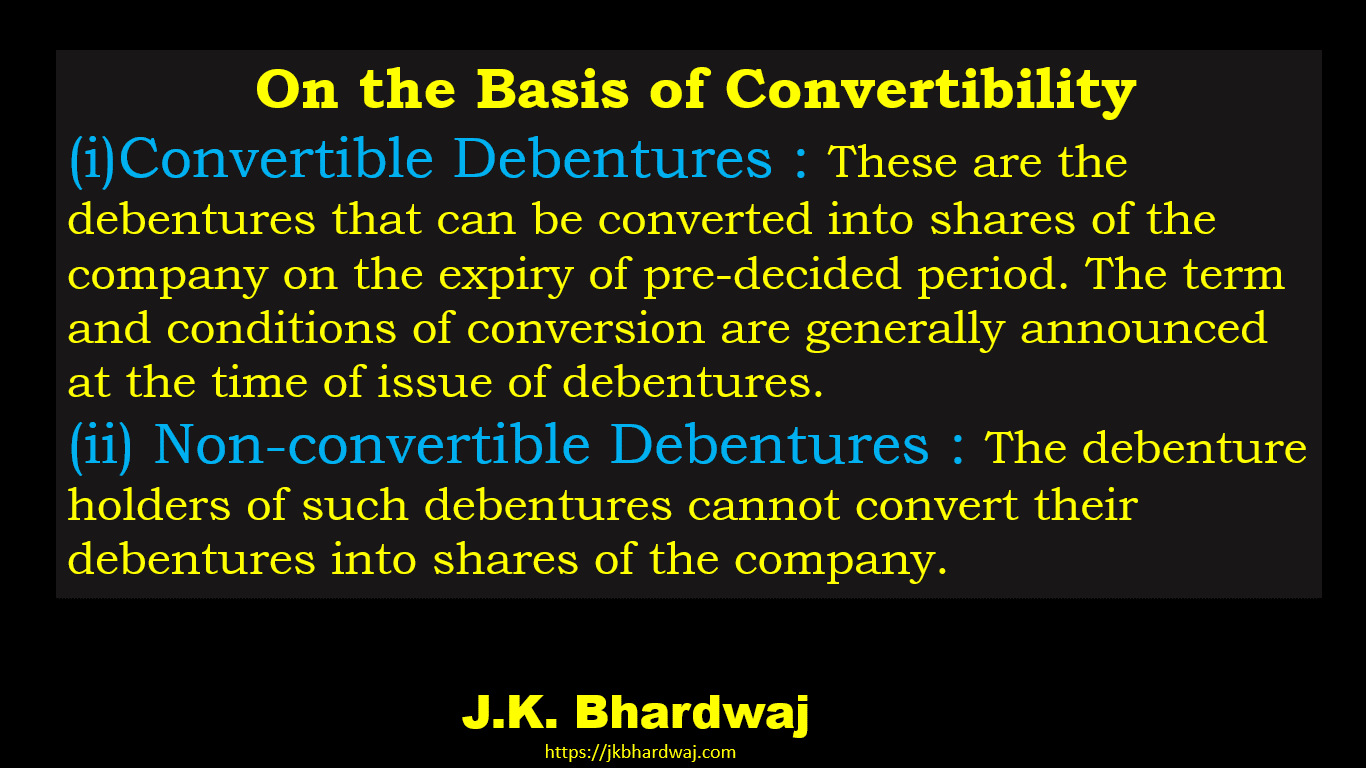

TYPES OF DEBENTURES: