20 transactions with their Journal Entries, Ledger and Trial balance

Table of Contents

20 transactions with their Journal Entries

Journal

A journal is one of the books of original entries in which transactions are originally recorded in a chronological (day-to-day) order according to the principles of the Double Entry System.

Transactions, when recorded in a Journal, are known as entries.

It is the book in which transactions are recorded for the first time. Journal is also known as ‘Book of Original Record’ or ‘Book of Primary Entry’.

This process of recording transactions in the journal is’ known as ‘Journalising’. Journal is also known as ‘Book of Original Record’ or ‘Book of Primary Entry’.

Business transactions of financial nature are classified into various categories of accounts

such as assets, liabilities, capital, revenue and expenses.

These are debited or credited according to the rules of debit and credit, applicable to the specific accounts. Every business transaction affects two accounts. Applying the principle of double entry, one

account is debited and the other account is credited. Every transaction can be recorded in the journal.

Also Read:

30 transactions with their Journal Entries, Ledger, Trial balance and Final Accounts- Project

Explanation:

- Date : In the first column, the date of the transaction is entered. The year and the month is written only once, till they change. The sequence of the dates and months should be strictly maintained.

- Particulars : Each transaction affects two accounts, out of which one account is debited and the other account is credited. The name of the account to be debited is written first, very near to the line of particulars column and the word Dr. is also written at the end of the particulars column. In the second line, the name of the account to be credited is written, starts with the word ‘To’, a few space away from the margin in the particulars column to the make it distinct from the debit account.

- Narration : After each entry, a brief explanation of the transaction together with necessary details is given in the particulars column with in brackets called narration. The words ‘For’ or ‘Being’ are used before starting to write down narration. Now, it is not necessary to use the word ‘For’ or ‘Being’.

- Ledger Folio (L.F): All entries from the journal are later posted into the ledger accounts. The page number or folio number of the Ledger, where the posting has been made from the Journal is recorded in the L.F column of the Journal. Till such time, this column remains blank.

- Debit Amount : In this column, the amount of the account being debited is written.

- Credit Amount : In this column, the amount of the account being credited is written.

LEDGER

Ledger is also called the Principal Book of Accounts.

After recording the business transactions in the Journal or special purpose Subsidiary Books, the next step is to transfer the entries to the respective accounts in the Ledger.

Ledger is a book where all the transactions related to a particular account are collected at one place.

A Ledger is a book which contains all the accounts whether personal, real or nominal, which are first entered in journal or special purpose subsidiary books.

According to L.C. Cropper,” The book which contains a classified and permanent record of all the transactions of a business is called the ledger.”

Posting

‘The process of transferring the entries recorded in the journal or subsidiary books to the respective accounts opened in the ledger is called Posting‘

RULES OF POSTING

*If an account is debited in the journal entry, the posting in the ledger should be made on the debit side of that particular account. In the particular column the name of the other account (which has been credited in the Journal entry) should be written for reference.

* For the A/c credited in the Journal entry, the posting in the ledger should be made on the credit side of that particular account . In the particular column the name of the other account (which has been debited in the Journal entry) should be written for reference.

Points to be Remember

‘To’ is written before the A/c s which appear on the debit side of ledger.

“By” is written before the A/c s appearing on the credit side.

Use of these words ‘To’ and ‘By’ is optional.

Balancing

Procedure for Balancing

While balancing an account, the following steps are involved:

Step 1 –Total the amount column of the debit side and the credit side separately and then ascertain the difference of both the columns.

Step 2 – If the debit side total exceeds the credit side total, put such difference on the amount column of the credit side, write the date on which balancing is being done in the date column and the words “By Balance c/d” (c/d means carried down) in the particulars column. OR

If the credit side total exceeds the debit side total, put such difference on the amount column of the debit side, write the date on which balancing is being done in the date column and the words “To Balance c/d” in the particulars column.

Step 3 – Total again both the amount columns, put the total on both the sides and draw a line above and a line below the totals.

Step 4 – Enter the date of the beginning of the next period in the date column and bring down the debit balance on the debit side along with the words “To Balance b/d” (b/d means brought down) in the particulars column and the credit balance on the credit side along with the words “By balance b/d” in the particulars column.

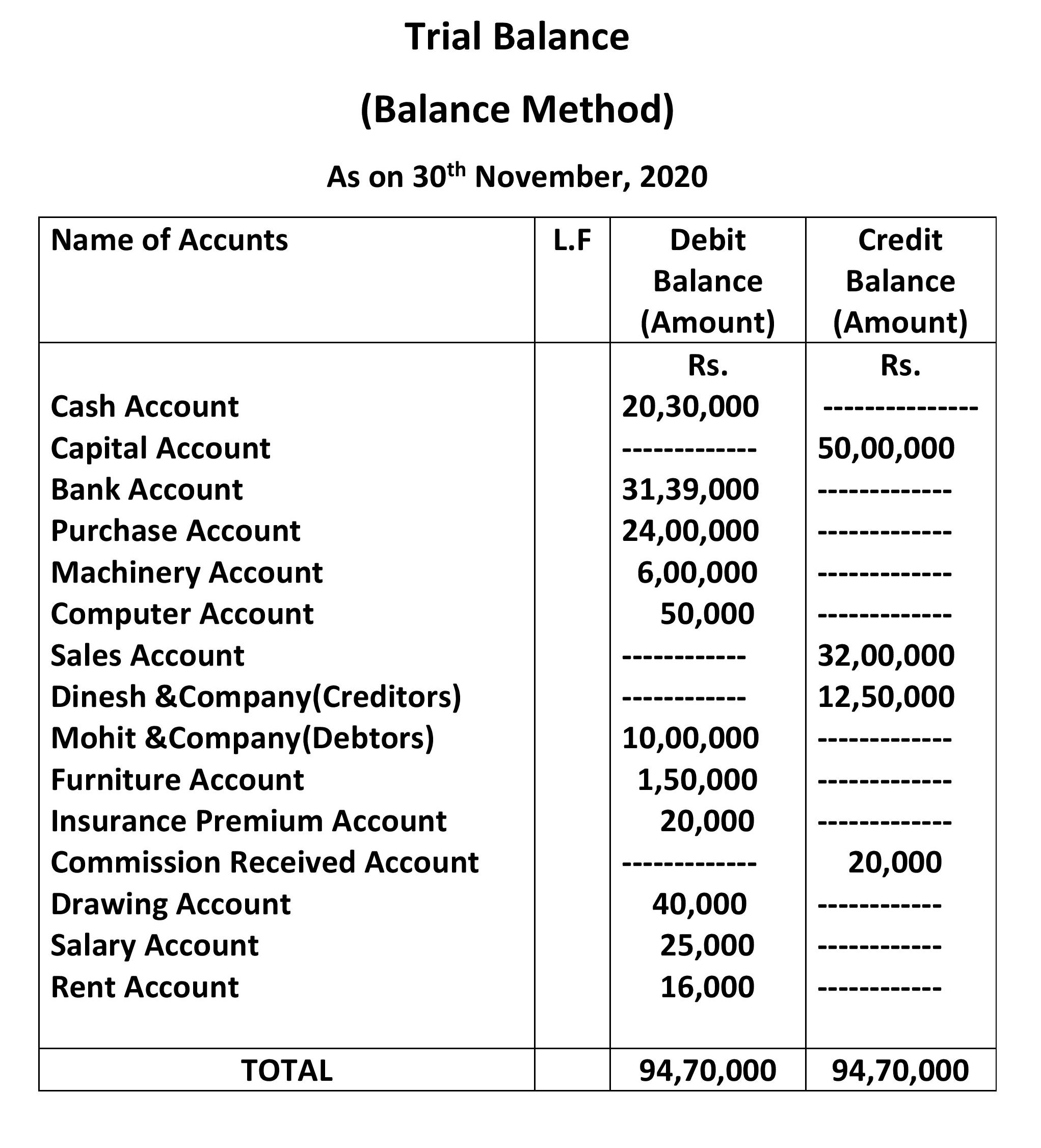

20 transactions with their Journal Entries: Trial balance

Trial balance is a statement prepared to check the arithmetical accuracy of the books of ledger accounts.

Trial Balance is the list of debit and credit balances taken out from ledger to test the arithmetical accuracy of the books. “It also includes the balances of Cash and bank taken from the Cash Book”.

First step recording of transactions in journal. The next step post them into ledger and the next step in the accounting process is to prepare a statement to check the arithmetical accuracy of the transactions recorded so for. This statement is called ‘Trial Balance’.

Trial balance is a statement which shows debit balances and credit balances of all accounts in the ledger. Since, every debit should have a corresponding credit as per the rules of double entry system, the total of the debit balances and credit balances should tally (agree). In case, there is a difference, one has to check the correctness of the balances brought forward from the respective accounts. Trial balance can be prepared in any date provided accounts are balanced.

20 transactions with their Journal Entries, Ledger, and Trial balance

Also read:

Diagrams for Circular flow of Income

Meaning and advantages of Double Entry System

Definition

“Trial balance is a statement, prepared with the debit and credit balances of ledger accounts to test the arithmetical accuracy of the books” – J.R. Batliboi.

Features of Trial Balance

- Trial balance is a list of the various ledger account balances whether debit or credit.

- It is prepared in the form of a statement.

- A firm prepares a trial balance in order to check the arithmetical accuracy of the ledger accounts.

- The arithmetical accuracy established by a trial balance is not proof that there are no mistakes in the books of accounts.

- A trial balance is usually prepared at the end of the accounting year. However, a firm may prepare it weekly, monthly, quarterly or half-yearly also.

- Trial balance does not form a part of the final accounts.

- It provides a summary of the ledger accounts. Thus, it serves as a link between the books of accounts and Trading & Profit and Loss A/c and Balance Sheet.

Objectives

- To check the arithmetical accuracy of the ledger accounts.

- Locate the errors.

- To facilitate the preparation of final accounts.

- Trial balance Provides the summary of Ledger Accounts.

Balancing of different accounts

Balancing is done periodically, i.e., weekly, monthly, quarterly, halfyearly or yearly, depending on the requirements of the business.

- Personal Accounts : These accounts are generally balanced regularly to know the amounts due to the persons (creditors) or due from the persons (debtors).

- Real Accounts : These accounts are generally balanced at the end of the financial year, when final accounts are being prepared. However, cash account is frequently balanced to know the cash on hand. A debit balance in an asset account indicated the value of the asset owned by the business. Assets accounts always show debit balances.

- Nominal Accounts : These accounts are in fact, not to be balanced as they are to be closed by transfer to final accounts. A debit balance in a nominal account indicates that it is an expense or loss. A credit balance in a nominal account indicates that it is an income or gain.

All such balances in personal and real accounts are shown in the Balance Sheet and the balances in nominal accounts are taken to the Trading and Profit and Loss Account.

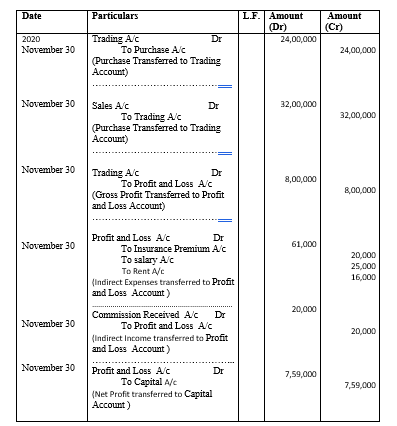

- Balance of Direct expenses Accounts are transfer to Debit side of Trading Account.

- Balance of Purchase Account transfer to Debit side of Trading Account.

- Balance of Direct Incomes(Sales) Accounts are transfer to Credit side of Trading Account.

- Balance of Indirect expenses Accounts are transfer to Debit side of Profit and Loss Account.

- Balance of Indirect Incomes Accounts are transfer to Credit side of Profit and Loss Account.

Financial Statements/Final Accounts

in 20 transactions with their Journal Entries

The statements that are prepared at the end of a particular accounting period to measure the overall result (Net Profit/Net Loss) of business activities and show the financial position of a business concern are generally called financial statements.

Or

The accounts which are prepared at the final stage (at the end of the financial year) of the accounting cycle to know the profit or loss and financial position of a business concern are called Final Accounts.

Final accounts gives an idea about the Profitabilitty and Financial position of a business to its management, owners, and other interested parties.

Financial statements/Final Accounts include these statements :

(i) Income statement (a. TradingAccount, b. Profit and Loss Account)—prepared to ascertain gross profit/loss and net profit/loss during an accounting period.

* Trading Account is prepared to ascertain the results of the trading activities of the business enterprise. Trading activities means buying and selling of goods. The trading account shows the result(Gross Profit/Gross Loss) of buying and selling of goods.

* Profit and Loss Account shows the net profit/loss during an accounting period. Profit and loss Account is an account, which is prepared to calculate the net profit or net loss of the business for the accounting period. Profit and Loss Account is a Nominal Account and as such, all the indirect expenses and losses are shown on its debit side and all the incomes and gains are shown on its credit side.

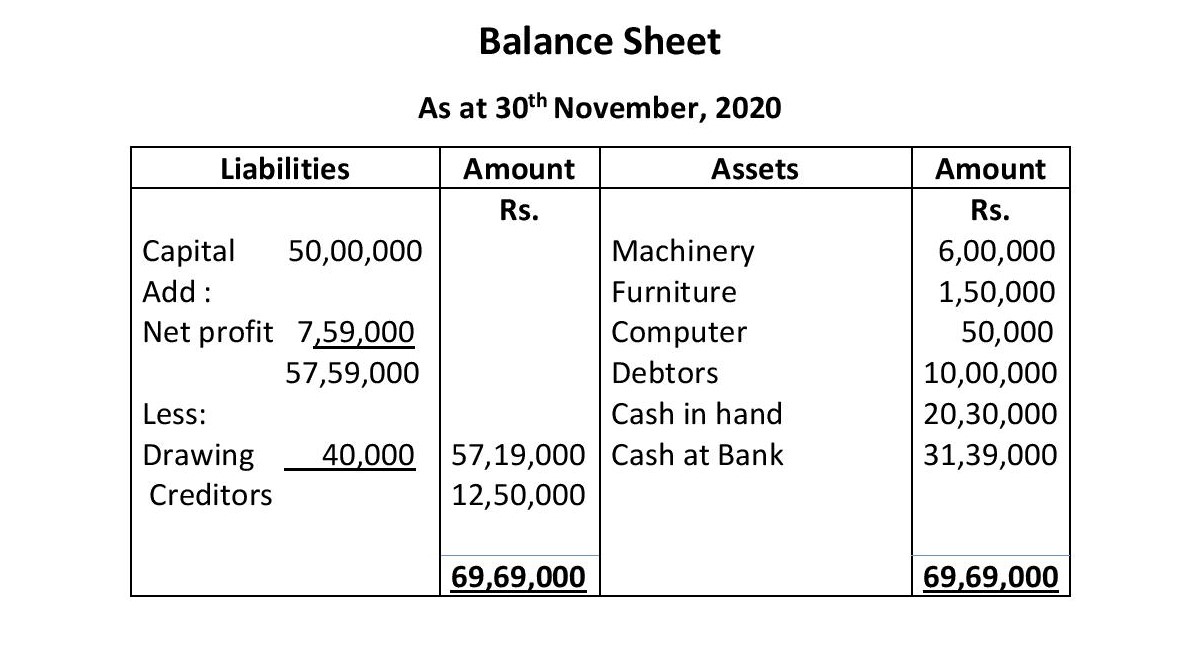

(ii) Statement of Financial Position (Balance Sheet)—prepared to ascertain Financial position (assets, liabilities and capital) of an enterprise at a particular point of time. Balance sheet is a financial statement that shows the financial position of a business and the nature and values of its assets and liabilities on a particular date.

- This forms the second part of the final accounts.

- It is a statement showing the financial position of a business.

- Balance sheet is prepared by taking up all personal accounts and real accounts (assets and properties) together with the net result obtained from profit and loss account.

- On the left hand side of the statement, the liabilities and capital are shown.

- On the right hand side, all the assets are shown.

- Balance sheet is not an account but it is a statement prepared from the ledger balances. So we should not prefix the accounts with the words ‘To’ and ‘By’.

Balance sheet is defined as ‘a statement which sets out the assets and liabilities of a business firm and which serves to ascertain the financial position of the same on any particular date’.(particular point of time).

Direct Expenses

Those expenses which are incurred on purchasing of goods and for converting raw material into the finished goods .

Or

Those expenses which are directly related to production/Manufacturing of goods or purchase of the goods are called direct expenses.

For Example- Manufacturing wages, Expenses on purchases (including all duty and tax paid on purchases, Brokerage on purchases of goods, Commission on purchases of goods), Carriage/Freight/Cartage inwards, Production expenses (such as power and fuel, water, coal,Gas etc.), factory expenses (e.g. lighting, rent and rates), Royalty based on Production etc.

Note : All direct expenses are debited to Trading account.

Direct Income

in 20 transactions with their Journal Entries

Direct income is the income which is directly retated to the particular business.eg, sales of the goods.

other words- Direct income is one which is earned directly by way of business activities.

Note : All direct income are credited to Trading account.

Indirect Expenses

Those expenses which are not directly related to production/Manufacturing or purchase of the goods are called indirect expenses. It includes those expenses which are related to office and administration, selling and distribution of goods and financial expenses etc.

For Example- Office & Admin. Expenses Salaries, Rent Rates Taxes, Printing and Stationery, Salaries & Wages, Postages and Telephones , Office Lighting, Insurance Premium, Legal Expenses, Audit Fees, Travelling Expenses , Selling & Distribution Exp. Carriage and Freight Outwards, Commission , Brokerage, Advertisement , Publicity Bad Debts Packing Expenses Salaries of Salesman Delivery Van Expenses ,Financial Exp. Interest paid on loans, Discounts Allowed Rebate Allowed Bank Charges Miscellaneous Exp. Repairs Depreciation on Fixed Assets Entertainment Expenses, Donations & Charity, Stable Expenses Unproductive Expenses

Note :These expenses are shown in the debit side of the Profit and Loss A/c.

Indirect Income.

in 20 transactions with their Journal Entries

Indirect income is one which is earned directly by way of non-business activities. eg- Profit on Sale of fixed Assets, Profit on Sale of Investment, Discount Received, Rent Received, commission Received, Interest Received,Dividend Received etc.

Note : All Indirect income are credited to Profit and loss account

Operating Expenses

An operating expense is a day-to-day expense incurred in the normal course of business. These expenses appear on the income statement.

Or

Operating expenses are the expenses which are incurred by the business in the normal course of its operations.

Or

Operating expenses are expenses a business incurs in order to keep it running, such Employee Benefit Expenses , Depreciation and Amortisation Expenses , Selling and Distribution Expenses, Office and Administrative Expense, Rent Tax and insurance etc.

Non- Operating Expenses

in 20 transactions with their Journal Entries

Such expenses that are neither related to normal course of activities of a business nor related to the production process of a business are known as non-operating expenses.

Non Operating Expenses = Interest on Debentures / Long Term Loans + Loss on sale of Non Current Assets

Non-Operating Incomes

in 20 transactions with their Journal Entries

Non-operating income is the portion of an organization’s income that is derived from activities not related to its core business operations.

Non Operating Incomes = Interest Received on Investment + Profit on sale of Non Current Assets+ Dividend received

20 transactions with their Journal Entries, Ledger, and Trial balance

PASS THE JOURNAL ENTRIES (WHICH SHOULD HAVE AT LEAST 20 TRANSACTIONS WITHOUT GST), POST THEM INTO THE LEDGER, PREPARE A TRIAL BALANCE BY BALANCE METHOD-

On 1st November, 2020 Mr.Rachit started a Readymade garments business in lalitpur Mr. Rachit invested Rs 50,00,000.

November 2 Cash deposited into the bank Rs. 30,00,000.

November 2 Goods purchased for cash Rs 8,00,000 at 25% trade discount .

November 3 Sewing Machinery Purchased for cash Rs. 5,50,000 and installation expenses paid Rs. 50,000.

November 5 Computer Purchased paid by cheque Rs. 50,000.

November 6 Goods sold for Cash Rs. 7,00,000.

November 10 Goods purchased from Dinesh & company Rs. 12,50,000 at 20% trade discount .

November 12 Goods Sold to Mohit & Brother Rs.20,00,000 at 40% trade discount .

November 15 amount paid to Dinesh & company by cheques Rs. 4,00,000.

November 16 Furniture Purchased paid by cheque Rs. 1,50,000.

November 18 Cheques received from Mohit and brother Rs 8,00,000 and deposited into Bank same day.

November 19 Goods purchased from Dinesh & company Rs. 10,00,000 at 20% trade discount .

November 20 Goods sold for Cash Rs. 5,00,000.

November 21 Goods Sold to Mohit & Brother Rs.10,00,000 at 20% trade discount .

November 24 Isurance premium paid Rs. 20,000 by cheque.

November 25 Cash received from Mohit and brother Rs 2,00,000.

November 26 Cash paid to Dinesh and company Rs. 1,50,000.

November 27 Commission Received Rs. 20,000.

November 29 Cash withdrawn for personal use Rs. 40,000.

November 30 Salary Rs 25,000, Rent Rs. 16,000 paid by cheque.

20 transactions with their Journal Entries, Ledger, and Trial balance

JOURNAL ENTRIES IN THE BOOKS OF RACHIT

20 transactions with their Journal Entries, Ledger, and Trial balance: Ledger Accounts

LEDGER

20 transactions with their Journal Entries, Ledger, and Trial balance

CLOSING ENTRIES

20 transactions with their Journal Entries, Ledger, and Trial balance

Admission of a partner-Important Questions-1

Important questions of fundamentals of partnership-3

Profit and loss Appropriation Account

Format of Profit and loss Appropriation Account

Hidden Goodwill at the time of Admission of A New Partner

Important questions of fundamentals of partnership

Important questions of fundamentals of partnership-2

Goodwill questions for practice Class 12 ISC & CBSE

Important questions of fundamentals of partnership-5

ACCOUNTING TREATMENT OF GOODWILL AT THE TIME OF ADMISSION OF A NEW PARTNER

20 transactions with their Journal Entries, Ledger, and Trial balance